I work in New York City as a Software Engineer. I earn a salary and use it pay for expenses such as rent, food, and things that make me happy. At the end of the month there is money left over, and this post explains where I put it to achieve my rough financial goals.

4-5 months expenses (based on 2 years of spending data) in cash in a Fidelity Money Market account currently paying 4.42%4.13% 3.28% interest (as of 19 June 2026)

Credit cards and other debt paid off ASAP

Maxed out 401(k) contributions and maxed out IRA contributions through a Backdoor Roth

The rest is auto-invested every Monday into Vanguard. 80% to VTSAX and 20% to VTIAX

In 2023 I came into a bit of money and became positively obsessed with personal finance. My setup is simple but a source of great pride to me. I’ve guided a few friends through this, so I thought it would be a better use of my time to write it down. Maybe you’ll find it helpful too.

The information in this post may not apply to you depending on your situation, but I believe it will apply to a large enough percentage of the people reading this. Details about me:

I am 32 years old and single.

I am a United States resident. I live in NJ and work in NYC as a Software Engineer.

I do not own my apartment (I rent).

My goals are to retire early, buy a home eventually, give my future children opportunities, and have money in retirement to buy - among other things - lots of FamilyMart egg sandos. I probably want to travel too, in those cool seats that recline to be completely flat.

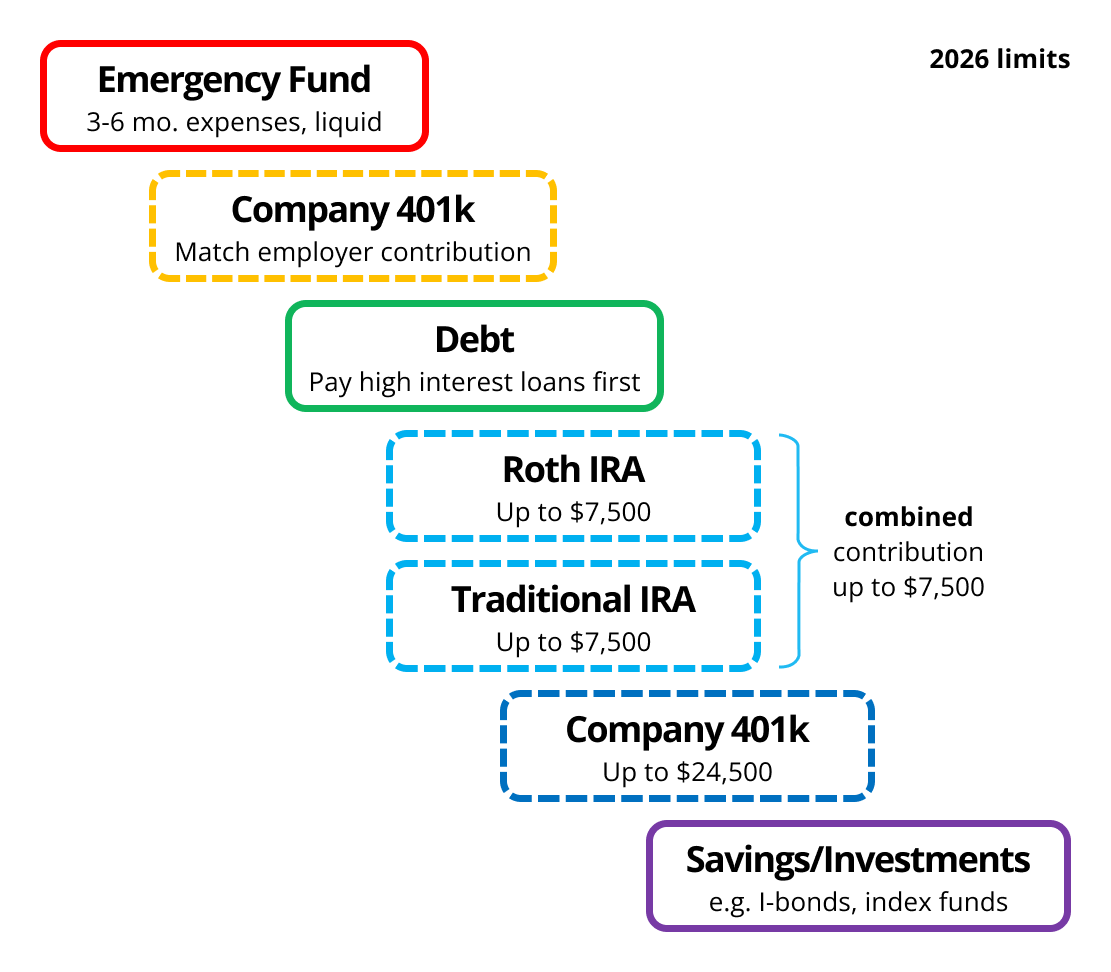

One important thing I focus on is “allocation priority.” That is, money needs to pay for X before it can pay for Y, or else I put myself at risk. This priority forms a sort of flowchart. There are more complicated ones online (search “personal finance flowchart reddit” for some goodies) but this one adopted from one I saw on r/bogleheads many years ago covers pretty much everything for me.

I keep ~4-5 months of expenses (rent + food + everything I spend money on based on 2-3 years of spending data) completely liquid in cash.

You need cash to pay bills and cover general expenses. If you don’t do this, bad things can happen, so it comes first. Before scratch-offs, before a secret stock tip, even before the safest of investments.

Note that this isn’t “cash” as in physical money under my mattress, but cash in a money market account on Fidelity, which currently pays me 4.42% interest. The balance in this account fluctuates slightly based on my spending throughout the year (gifts, angel investments, etc.) so I keep an eye on it and adjust later sections of this flow-chart accordingly.

I use this money to pay rent, my credit card bills, and the occasional ACH/wire transfer. I use Fidelity because their money market accounts refund ATM fees and give me a number account/routing number combo.

I keep a Name Brand bank account around for convenience, but Fidelity has largely replaced it.

You can use a normal checking account (potentially very low / almost criminal interest) or a number of other money market or high yield savings options.

Note: “Matching” is the important part here, and the focus of this step, I’ll write a bit about the 401(k) in a later section.

My employer matches 4% of my salary in 401(k) contributions every pay period, so every paycheck I contribute at least 4%×My salary/24 pay periods to a 401(k), where it is matched dollar-for-dollar.

This is a 100% return on investment, which is a higher rate than the stock market and, controversially, a higher rate than many loans. This is why it’s the second step in the flowchart, do this early!

Check if you have 401(k) matching at work, and check if it’s every pay period (in which case you need to contribute every pay period) or some other matching schedule (maybe you can drop a few grand into your 401(k) on Jan 1st and not think about it).

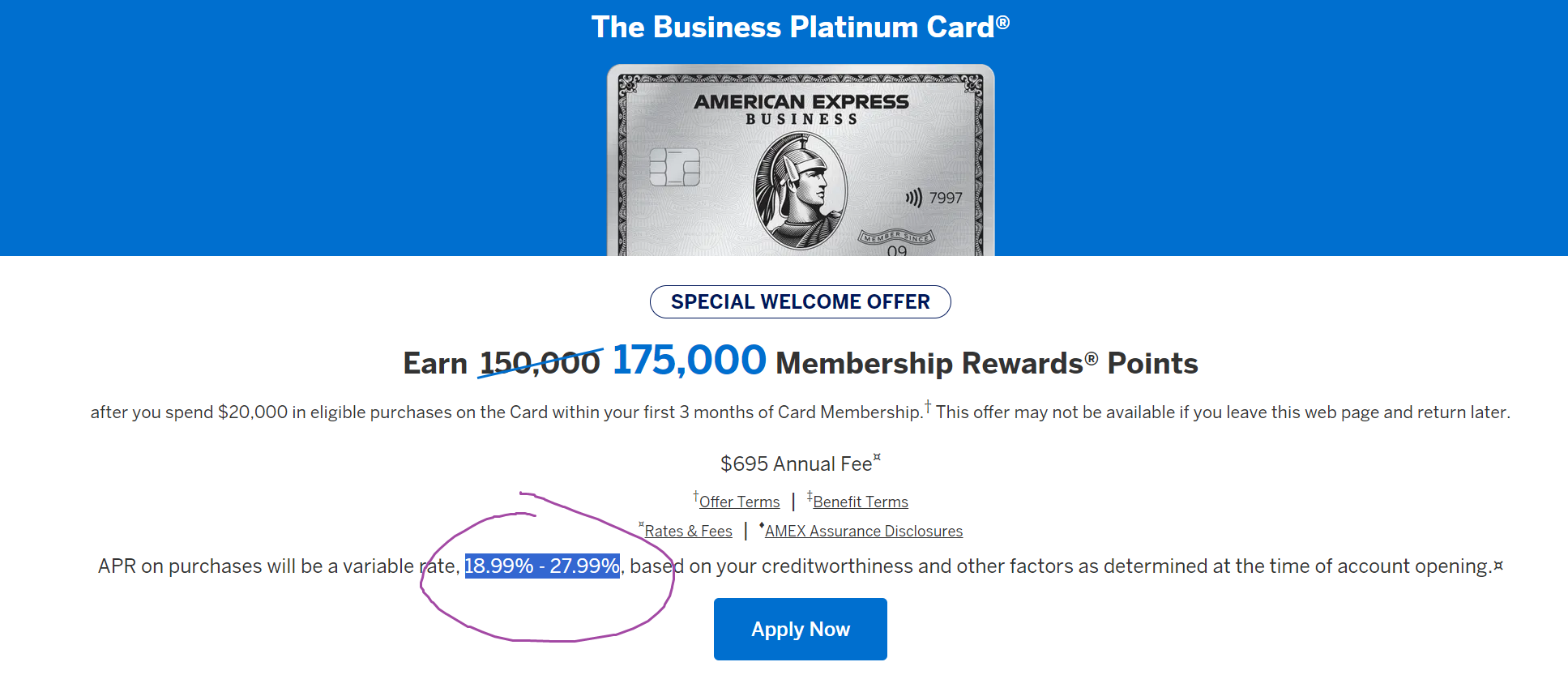

Your credit card interest is very high. This means your balance is becoming ~20% more expensive every year. This is a higher rate than the stock market will likely return (depending on whoyouask), so you should really pay it off before investing in the market.

The Amex Platinum card has an APR anywhere between 18.99% and 27.99%. This is why they can offer you sweet deals on business class travel (

Credit card rewards points).

If you’re currently paying off a TV with credit, every dollar left on the purchase of that TV is turning into ~$1.28.

Every dollar you’re putting into the stock market instead of towards this debt is turning into, on average, $1.07-$1.10 (depending on whoyouask) You also have to pay taxes on these gains. The TV is outpacing you!

Every dollar you’re instead spending at the roulette wheel is turning into $0.94. Whoops, we went the wrong way.

Depending on your employment status and income , you can contribute (in 2025) $23,500 towards a tax-advantaged 401(k) account and an additional $7,000 into an IRA.

I like to group these two categories together under a single “retirement” bucket, but IRAs are more flexible (access to more funds, including ones with lower fees) so they often get listed first in priority.

At my day job, I have access to a 401(k) plan like many other private-sector American workers. This is an account I can (in 2025) contribute up to $23,500 per year with tax benefits:

The “Traditional” option where this $23,500 is deducted from my taxable income (money that is taxed at around 40% in my bracket).

The “Roth” option where it is not deducted (I am taxed on it) but withdrawals are tax-free

I like the Traditional option because my current tax rate is high (both the income bracket and the state I work in). Talk to an accountant or money-smart family member to figure out which one is better for you. I spread this amount over each paycheck.

Additionally, you may be able to contribute $7,000 more towards an IRA. If your income is too high you may be able to leverage the Backdoor Roth. Talk to an accountant to help you set this up if you’re unsure. I do this every year in early January.

The tax incentive is why these contributions appear before our later priorities (personal brokerage, crypto, scratch-offs, scams, etc.). Take advantage of them!

Which funds should you invest in? Your 401(k) provider may have limited options (or even just a stock/bond split), but the next section (though it concerns taxable contributions) can help in cases where you have flexibility.

Congrats on making it this far! Anything extra is yours to play with. I like to invest my extra in index funds, and occasionally light $5,000 checks on fire through angel investments.

If you’ve got cash for emergencies, bad debt is paid off, and your retirement contributions are maxed out — it’s now time to have fun and invest your money how you want. What I like to focus on at this point are three things:

The risk factor of my investments (scratch-off tickets vs. Treasury bonds)

The fees of my investments (who is getting rich off my money)

The taxes I’ll be paying on gains (namely: short-term vs long-term capital gains tax)

One of the simplest contributions you can make is a Target date fund. This is a fund that will auto-balance its stock/bond allocation based on your target retirement date.

The fees are generally quite low: Vanguard’s 2055 retirement fund, VFFVX, has an expense ratio of just 0.08%. With an investment of $10,000 per year you’ll be “paying” about 8 bucks. (Note: This is priced into the fund and will not show up as an actual fee anywhere).

“Robo-investors” (such as Wealthfront and Betterment) have emerged in the past decade to also serve this need. Their fees might be a bit higher, even with some crafty tax-sheltering strategies. Making fancy apps and being a billion dollar startup doesn’t come cheap!

If you’re a nerd like me and love spreadsheets, you may just want to do this all yourself. I like to put all my investments in an 80/20 Three-fund portfolio. Every Monday I auto-invest a dollar amount I’ve tweaked based on Priorities 1-5 (too high and I won’t have enough cash, too low and I’ll have too much cash) into Vanguard where it sits and grows. 80% of this goes towards VTSAX and 20% goes towards VTIAX.

I do not withdraw this money.

I rebalance every 6 months or so, or when a decent amount of cash comes in.

You can also have fun! You can invest in individual stocks (thrilling but risky), I-bonds (protected by inflation), crypto (probably a bad idea), scratch-offs (almost certainly a bad idea), or write angel checks (probably the lowest return on investment of them all but really fun).

Update (Dec 2024): I have since changed my auto-invest schedule from every Monday to twice the amount every other Friday (pay day at my current employer). This ensures as much money is in the market for as long as possible. I don’t believe there’s a huge difference, and weekly contributions are probably what I’d recommend for simplicity’s sake.

Personal finance is a deeply personal journey, but I hope the information in this post can help you on that journey. The contents of this article are inspired by lots of conversations with friends, family members, and some books which I’ll link below (note: the following contain Amazon affiliate links):

Little Book of Common Sense Investing by John C. Bogle the creator of the world’s first index mutual fund. I like this book because it spends a lot of time talking about fees and why indexing works.

A Random Walk Down Wall Street by B Malkiel. My favorite part about this book is the chapter(s) on “chartists,” or people who claim to notice movements in the markets by looking at their graphs. He gives quite a charitable review of them!

The Simple Path to Wealth by JL Collins, a well-known personal finance blogger. I loved this one because it gives tons of practical advice and is incredibly easy to read. The prose in this post is clearly inspired by Collins.

If you have any questions or feedback on this post, I’d very much love to hear it! me@jordanscales.com. Thanks so much for reading.

and maxed out IRA contributions through a Backdoor Roth

and maxed out IRA contributions through a Backdoor Roth

Credit card rewards points).

Credit card rewards points).

me@jordanscales.com. Thanks so much for reading.

me@jordanscales.com. Thanks so much for reading.