Have I saved enough for retirement?

Comparison is the thief of joy, and nowhere is that more obvious than in personal finance. Instead of figuring out your goals and focusing on improving your situation, many choose to compare themselves to their peers.

I take great issue with this, specifically when it comes to retirement savings.

People often ask, “I am X years old; how much should I have saved for retirement?” I find this question to be — to be blunt — completely meaningless. The short answer is: You can’t go back in time and save more, so focus on saving as much as you can.

In

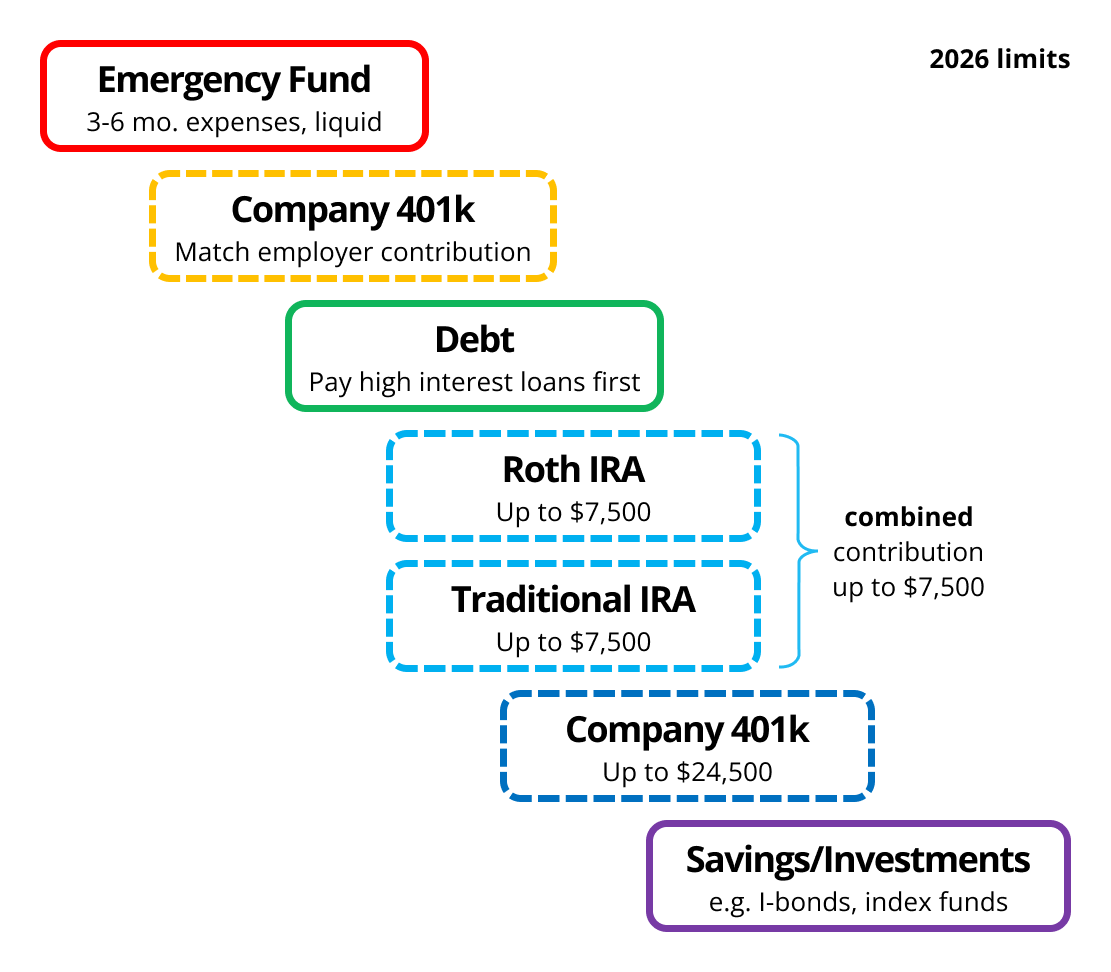

Where I put my money I elaborate on the “order of operations” for where to put savings. Check off the most important boxes first and make your way down toward financial independence. I make the case that, because of the tax benefits, saving for retirement is a good idea.

Where I put my money I elaborate on the “order of operations” for where to put savings. Check off the most important boxes first and make your way down toward financial independence. I make the case that, because of the tax benefits, saving for retirement is a good idea.

Where I put my money I elaborate on the “order of operations” for where to put savings. Check off the most important boxes first and make your way down toward financial independence. I make the case that, because of the tax benefits, saving for retirement is a good idea.

So, you’re 35 years old, and you’re looking at your 401(k) balance. Then you read an article that says you should have one year’s salary saved.

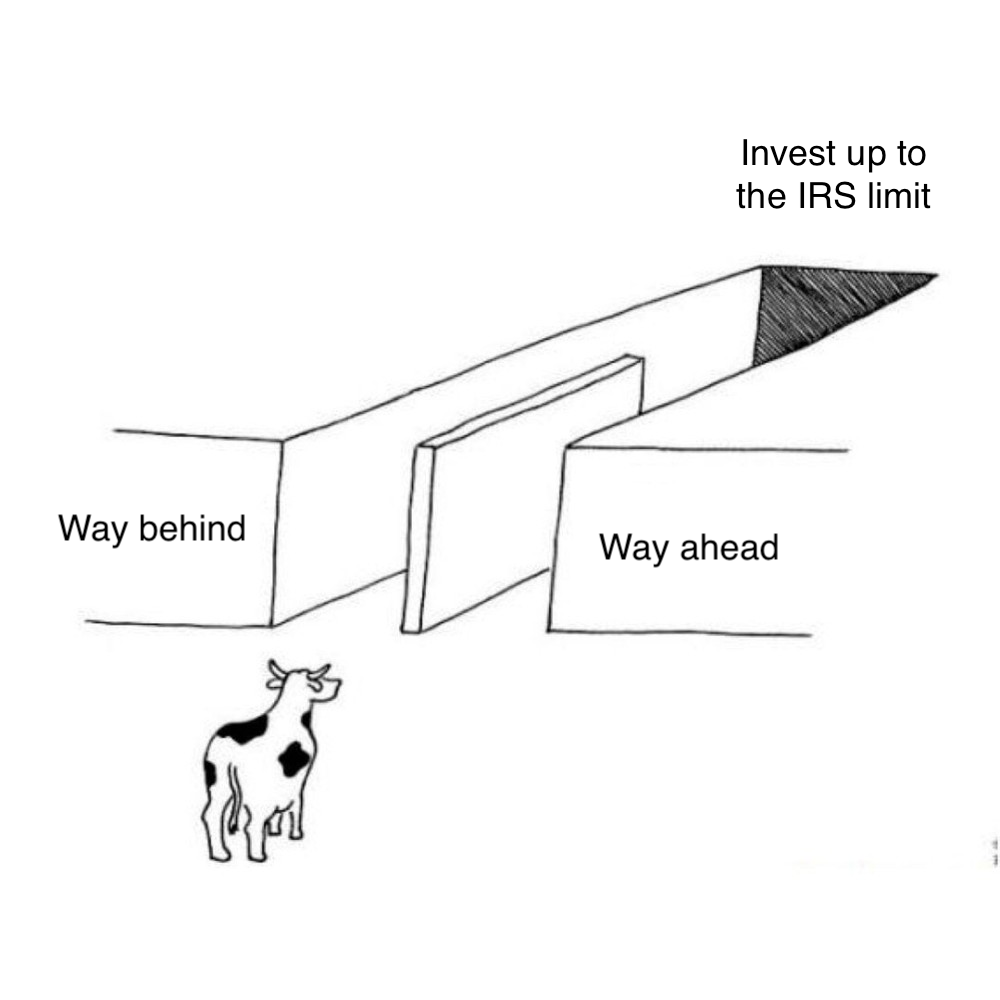

If your balance is lower than that, you might be disappointed; you might feel “behind.” What should you do?

Can you go back and invest more to get yourself caught up to a year’s salary?

No. The IRS imposes a limit. If you’re $100,000 behind your target, you simply cannot catch up to it this year. But don’t give up. Do the most you can do — save as much as you can.

What if the opposite is true? What if you’ve been contributing since your first working years, propelling you far beyond “one year’s salary”? Should you stop contributing?

No. You contribute for the tax benefits, not to appease an article. Instead, you should save as much as you can.

So, if you’re under the “suggested balance” you can’t catch up, and if you’re above the “suggested balance” you shouldn’t slow down. Regardless of where you are, you should save as much as you can for retirement.

Comparing yourself to a blog post, including this one, isn’t worth your attention.